What is real estate loan refinancing, and how to do it

Фото: Depositphotos

First of all, what is refinancing? In simple words, this is when you have real estate and a loan for it, and you want to take out a new loan with better conditions and pay off the previous one in full. By the way, refinancing can be not only for housing, but also for a car, business, yacht, and so on. For something that has a price, writes Andrey Boychuk in an article for Immigrant porada.

What does “with better conditions” mean, and is it worth doing? With better conditions means you will save financially. The interest rate on a bank loan fluctuates every day. For example, when you took out a loan, you took it at 10%, and today the loan rate is 5%. If you refinance, you can save money. Whether to do this or not depends on your situation, you need to do the math.

By the way, refinancing is not a free service. From $1000 and above. So, in New York it will cost you $4000-$8000. Unfortunately, I cannot give you a specific price, because there are many nuances in this process, and the laws of the state where you live also affect. I refinanced in December 2015 on the house I live in and it cost me $4500. So I think the best way is to show you the real numbers so you can see how much it costs and what the benefit of refinancing is. At the end of the article I will write all the numbers that I actually got.

I did refinancing for the first time, so I will describe step by step for those who plan to do it now or in the future.

How to start refinancing?

You made the calculations and realized that you need to refinance. What's next? Where to begin? Let's start with your goals. What is your goal for this accommodation? Answer the following questions:

- Are you planning to live in this place all your life?

- Do you plan to live here until 15 years?

- Do you plan to live here until 5 years?

Depending on your answers, you will need to choose loans. My wife and I decided that we would still live in our house for about 3-5 years. Therefore, it made sense for us to make the so-called 5 / 1 arm loan. This is a loan in which the loan rate is the lowest among others. But the risk is that in 5 years the percentage of my new loan may increase or decrease (as a rule, of course, it increases).

The interest rate can only be raised once a year and can only be done 2 times over the life of the loan after 5 years. For example, new loan 5 / 1 Arm from 2,5% in the first 5 years, then rose to 3,5% in the sixth year and, say, again to 4,5% in the seventh year. Now the percentage of 4,5 will be held to the end, until I fully pay (30 years).

Choosing a bank for a real estate loan

So, you have decided on the loan you want to take. Now you need to find a bank with the most favorable conditions. Do not be emotional in this matter: for example, I will go to Chasebecause in this bank I have an account or I like its logo more. It sounds ridiculous, but there are such people. And I am no exception! I can only like a company because it represents itself. But this is not always correct.

Be logical. If the second bank offers you better conditions than the first, then take a loan in the second bank. I recommend it the way I was advised, and as I myself did. Contacted 3-4 banks. Received from each of them all the necessary information, the percentage of the loan, how much is the paperwork. He compared all the numbers and chose a bank with a favorable rate, chose the cheapest option. But that is not all.

Now, contact all the banks, except for one (the one that offered you the best conditions) and ask if they can give you the same, only better. In my case, everyone refused. But this does not mean that you will not succeed!

As a result, I chose a bank, which was in second place, but to be honest, I did it only because I was confident in the success of the enterprise, because one of my friends who worked at the bank helped me in this matter.

Фото: Depositphotos

Filing documents

After I gave the go-ahead, they sent me a list of documents and forms that I filled out and signed. And here a small problem arose. My friend from the bank called me and said: “Andrey, your credit history and salary are wonderful, you have everything you need. But on your account (we were talking about checking accout. - Author) indicated $25 in the monthly report.” By the way, to your checking accout I always use, and my amount varies from 0 to several thousand there, so I do not attach much importance to it. But for the bank, it turns out, it matters. Hmmm ... A friend of mine asked if I had a savings account (saving account) and is there money there? Yes, of course there is. So I sent in statements for my existing savings accounts, and the problems disappeared.

Lawyer and title company

After I filed all the documents, I had to find a lawyer and title company (a company that checks ownership of real estate). Here again I wanted to check several options to compare prices, but I was too lazy (which, by the way, is very bad, because in those moments when you are lazy, do you lose money?).

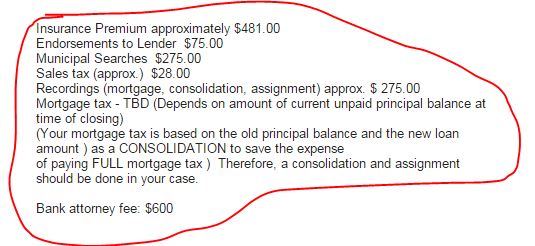

Therefore, I asked a lawyer and immediately title company (2 in the same office), how much will it cost. They said $ 1734. Here are the details:

Then I asked my friend from the bank if she could recommend someone for Staten Island. She gave me a man, but he was not interested in working with me. First, he told me for his service, the price in 2 is more than the previous lawyer, and still had to pay title company. Then I tried to bargain some more $ 50-100. But this lawyer stood firmly on his price and did not lower the price even for a dollar. I agreed with them all the details and said that I wanted to hire him. After that I sent the contact information of the representative of the bank, and they already did all the business among themselves.

Document Analysis

In total, the whole process took six weeks. Nothing was demanded of me, except to sign, perhaps one or two forms, which I received by mail. Then, when everything was ready, all documents were sent to title company and a lawyer. I met them at their office, where we signed a million different documents, moreover, in 2 or 3 copies. Poor trees.

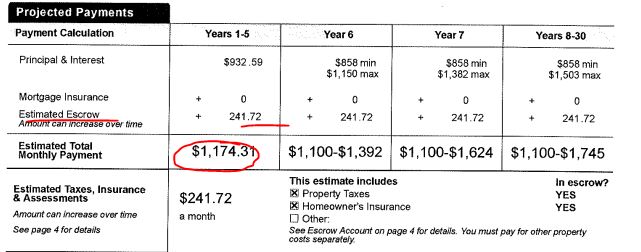

I will not share all the documents with you, because you will be tired of reading and viewing, but I will show the main one, in my opinion, because it is accessible to everyone. The first part is how much loan you take out and how much you will pay on the loan per month: interest + balance. But wait, not only this, but also something else. See part two.

Your monthly fee also includes a tax for land and property insurance. Therefore, the final payment amount per month will be $ 1 174.31. By the way, these are real numbers on the contract, nothing has been invented here. Yes, you can have a house in New York for such money a month.

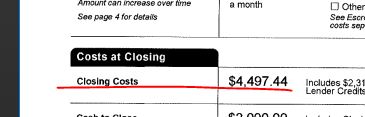

And one more thing - how much we have to pay for the entire process of paperwork. By the way, we didn’t pay out of our own pockets, but simply took it all into account in the loan. Therefore, this $4497 is already included in $221.

By the way, before meeting with the lawyers, somewhere for the 1-2 of the day, my previous loan was fully paid by the bank, which gave me a second loan. This is the essence of refinancing: to close the first loan and open another one. One problem arose in the fact that I had set up automatic payments in the bank, and I set them up for a new one. I thought that they automatically stop the previous automatic payments, but it turns out that these are different departments in the bank and they have not done so. Therefore, I have already paid for a loan that was not there, and they returned the money somewhere through 3-4 weeks. So keep this in mind; do not make a similar mistake.

And one more thing for any new loan. Try to pay once every two weeks, and better automatically. Why? If you pay 2 once a week, instead of 1 once a month, the loan term is reduced by about 2-3 years, that is, from 30 to 27-28 years.

The result of my refinancing

Finally, compare my costs and how profitable it was.

Our old payout amount was $ 1 550.00

Our new loan payout — $1

We paid for refinancing. $ 4 497.44

Savings per month - $ 376

That is the cost of refinancing will pay off in 12 months.

Was it worth it? Yes, because if we plan to live in this house for another 3-5 years, we will save $9 - $024.

About the Author: Andrey Boichuk - founder Immigrant porada (iporada.com) - platforms for Ukrainian immigrants in the United States. Cheerful husband beautiful wife and father of a joyful daughter.

This blog is translated from the Ukrainian language. The original article can be found on the website. "Immigrant Porada" (Ukrainian online advice platform for immigrants in the United States).

ForumDaily is not responsible for the content of blogs and may not share the views of the author.. If you want to become the author of the column, send your materials to [email protected]

Read also on ForumDaily:

15 ways to increase your income

11 steps when buying a home in the USA

10 US major cities where real estate prices fall

Top 10 expensive cities in the US

Top 10 cheapest cities in the USA

Subscribe to ForumDaily on Google NewsDo you want more important and interesting news about life in the USA and immigration to America? — support us donate! Also subscribe to our page Facebook. Select the “Priority in display” option and read us first. Also, don't forget to subscribe to our РєР ° РЅР ° Р »РІ Telegram and Instagram- there is a lot of interesting things there. And join thousands of readers ForumDaily New York — there you will find a lot of interesting and positive information about life in the metropolis.

-

Where in the USA to buy the medicines we are used to: a list of pharmacies5330

-

Six ways to cut your medical bill in the US436

-

Joy to Work: 37 Jobs with Lowest Stress and Good Pay419

-

What folk remedies treat the common cold in the USA: what surprises our354

-

Personal experience: why immigrants have more chances of success in the USA than Americans290

-

Burger Arthritis: How Fast Food Triggers Autoimmune Diseases233

-

XNUMX stunning US lavender farms that will take you to French Provence220

-

Actions in a terrorist attack: how to survive yourself and help others6333

-

Where in the USA to buy the medicines we are used to: a list of pharmacies5330

-

How to hit the jackpot: tips from a man who won the lottery 7 times4898

-

Life after death: what happens to places of mass executions in the USA3883

-

How to start a profitable business in the USA, if you have only $ 203281

-

4 US Social Security Traps and How to Avoid Them1493

-

Street, avenue, boulevard or drive: how to understand the classification of US streets and roads1461